Summary

- Surging global demand for critical raw materials has strengthened the bargaining power of resource-rich African countries. They are introducing new local content obligations for foreign mining companies that wish to operate in their territory, such as requiring the use of local goods and hiring local workers.

- The EU needs a secure and stable supply of critical minerals from Africa to power its green transition. However, its approach to this lags behind major players such as China and Gulf states, especially regarding investments in mining and processing ventures.

- European leaders should deepen their diplomatic efforts to encourage African countries to take a regional approach to imposing local content obligations. Greater economies of scale and cross-border activity would help improve resource-driven economic diversification in Africa.

- Europeans can distinguish their offer by providing grants or subsidies to EU-based private sector mining companies to invest in African STEM education and innovation, including establishing mining research centres.

- Europeans can also set themselves apart by supporting enterprise development strategies that include targeted training on competitiveness and accessing markets, obtaining financing, and other business development services.

Mineral geopolitics: A golden opportunity for African industrialisation

Africa has become a hotbed of geopolitical competition over critical raw materials (CRMs). These are the essential ingredients that will power tomorrow’s economies, found in solar panels, wind turbines, electric vehicle batteries, and more. Many outside players are now seeking to access Africa’s prized resources, including traditional partners such as the United States, the European Union, and China, and emerging economies such as the Gulf states, Turkey, and India. In the past two years, private and state-backed companies from these countries have snapped up new mining rights, secured concessions, and unveiled plans for mineral processing plants, refineries, and battery production facilities right across the continent.

Surging global demand for CRMs has handed some African governments newfound bargaining power. Resource-rich African countries now oblige aspiring partners to accept demands that they hope will drive domestic innovation and productivity and help build sustainable industrialised economies. Many states have already brought in export bans on unprocessed ores and introduced local content requirements, which mandate the use of domestic goods and services in value-added processing and guarantee a certain proportion of domestic ownership. African policymakers’ goal is to encourage the benefits of these CRM investments to be felt in other sectors of the economy. They aim to retain more wealth within their countries and raise Africa’s global share of value-added manufacturing well above its current level of just 2 per cent.

With such requirements becoming a non-negotiable part of the African offer, Europeans – along with their competitors – must comply with Africa’s fast-changing regulatory landscape. At the same time, the EU remains almost entirely reliant on China for its supply. As geopolitical competition deepens, the bloc is under pressure to de-risk by securing alternative sources. Yet European plans are falling short in their ambition to work with the private sector in African countries to build refining and smelting facilities and embark upon downstream projects. The EU intends flagship initiatives such as the Lobito Corridor to act as a counterpoint to Chinese influence. Some new infrastructure has resulted from European efforts. But this type of initiative reinforces a ‘mine-to-port’ narrative of an extractive relationship that is unappealing to African decision-makers. From their perspective, the geopolitical dilemmas preoccupying Brussels or Beijing are of little interest. Their wish is to form strong partnerships with whoever is willing and able to help their countries industrialise. African governments will leverage any and all opportunities presented by the CRMs boom. This gives the EU and its member states the chance to secure a more sustainable foothold than they have so far achieved.

This policy brief argues that meeting local content requirements is critical to unlocking the potential of the EU-Africa partnership. It proposes ways to make these obligations work within the EU-Africa mining partnership. The paper shows how European firms can cooperate with African countries on local content obligations both to foster local industrialisation for Africans, and secure access to CRMs for Europe in a way they have so far struggled to do. Specifically, it identifies five challenges within existing EU-Africa CRM relationships and suggests ways for Europeans to solve these to the benefit of both sides. It further argues that the entrenched presence of China in many parts of the CRM value chain across the continent means that Europeans cannot ‘compete’ directly – but that they can secure access of their own, and make some attractive offers that other powers are unable or unlikely to make.

Home is where the CRMs are: Evolving regulations in Africa

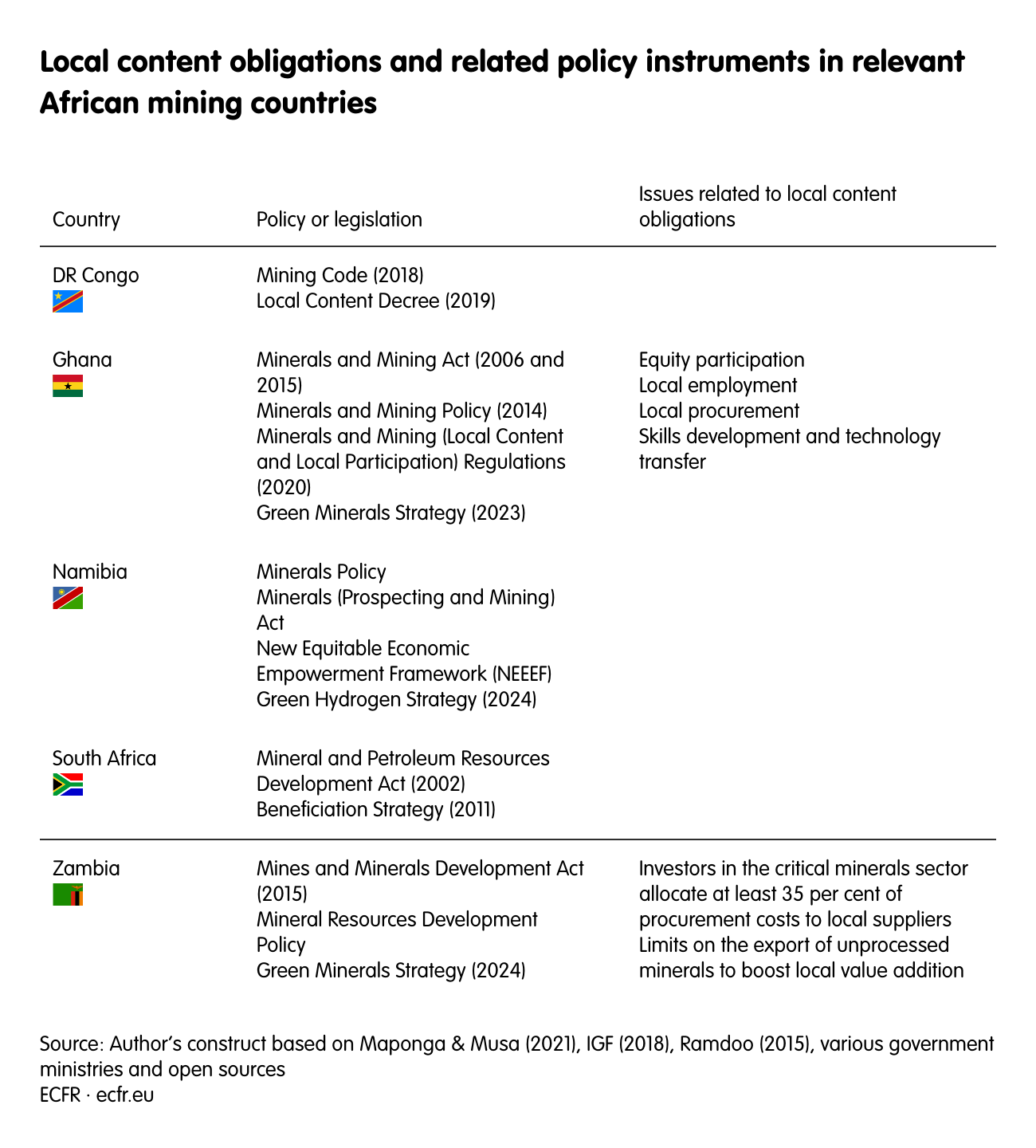

Many African governments and policymakers see a once-in-a-generation opportunity to industrialise by capitalising on the global demand for CRMs. Countries such as the Democratic Republic of the Congo (DRC), Ghana, Namibia, Zambia, and Zimbabwe have already enacted policies and strategies to ensure the mining industry is at least partly locally owned and supplied. At the same time, the African Union is upgrading protocols and instruments such as the 2009 Africa Mining Vision and the 2018 African Minerals Governance Framework, whose purpose is to guide the industrialisation of African countries by leveraging their mining endowments. The African Development Bank is championing a new African Green Minerals Strategy focused on beneficiation and industrialisation.

For Europe, this means that African countries will likely continue imposing local content obligations regardless of where the investment comes from – be it north America, Australia, the EU, China, or the Gulf. African governments will no longer tolerate the old ‘extractivist model’ of exporting raw materials without obtaining local added value. The continent has what the world increasingly wants. This gives African countries strong bargaining power and a huge opportunity to boost their resource industries and their economies more generally.

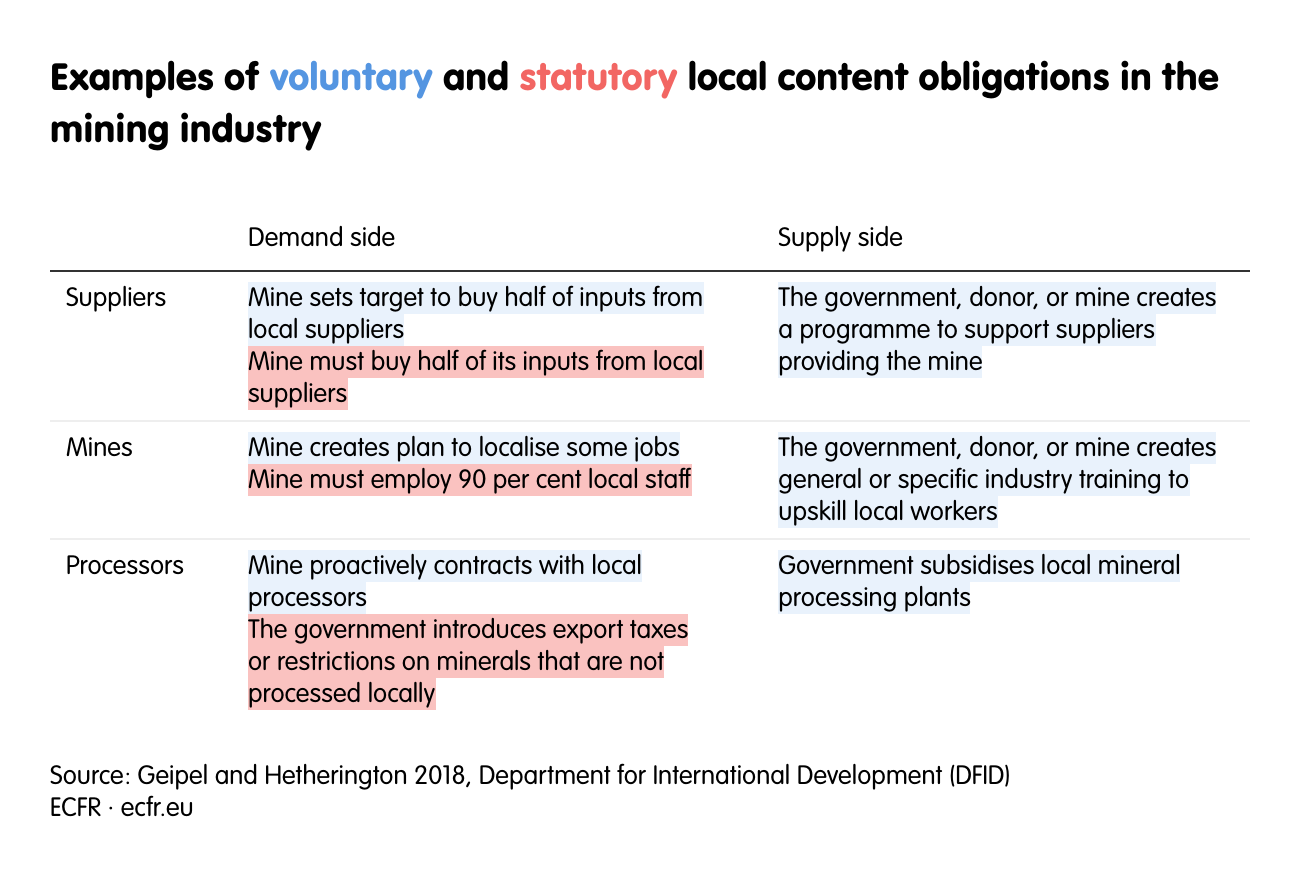

Local content obligations

Local content obligations refer to a set of policy instruments that governments use to achieve goals such as: ensuring some domestic ownership of the CRM mining industry; and requiring that the mining industry uses local economy supplies for a proportion of factors of production, such as labour, goods and services, technology, and technical know-how. African policymakers’ aim is to encourage the growth of mining ventures to spill over into the rest of the local economy by retaining some profits, ensuring forms of local ownership of mines (known as equity participation), and creating linkages with other sectors. These linkages should include sectors beyond CRMs and mining. Together, these efforts intend to increase revenue, jobs, and opportunities to upgrade skills and technology in the host country.

In response to the rising global demand for CRMs, over the last decade the DRC, Ghana, Namibia, and South Africa have taken the opportunity to introduce local content obligation legislation. In practice, these local content policies largely focus on equity participation, local procurement, employment quotas, skills development, and technology transfer. Zambia is also seeking to introduce legislation requiring that at least 30 per cent of the production of critical minerals from future mines be owned by the state and that investors in CRMs allocate at least 35 per cent of procurement costs to local suppliers.

Often, securing partial local ownership of the mine by national or state-owned companies is the easiest entry point for the state to achieve the equity participation aspect of these local content obligations. This is on display in countries such as Ghana, Uganda, South Africa, and Zambia, where state-owned mining companies or sovereign wealth funds have direct equity in mining ventures.

Nonetheless, meeting the requirement to build linkages with other economic sectors can be challenging in many African countries. This is partly because of the lack of domestic suppliers able to fully participate in procurement markets, which is in turn due to the limited availability of locally made goods, workers, and technology in both private firms and government agencies. Other impediments include the lack of available local funding for research and development and innovation activities, the weakness of available incentives such as tax waivers, and insufficient electricity supply for value-addition processing. Indeed, most CRM-rich African countries lack the necessary infrastructure – such as power, railways, and roads – to make their value-addition production globally cost-competitive. Some studies show that African countries could become cost-competitive in refining raw materials by 2030 by leveraging access to mines, low-cost electricity, and inexpensive labour. While the industry cites these factors as mitigating against meeting local content and broader diversification goals, resource-rich governments still push for local content.

Nevertheless, some African countries have succeeded in imposing obligations on foreign mining companies, requiring them to use local businesses to provide goods and services to the mining sector. For example, in December 2020, Ghana adopted regulations that include a procurement list of 50 crucial items, such as explosives, which must be sourced using Ghanaian procurement and supply chains. Only companies with solely Ghanaian directors and shareholders can supply specific items integral to mining, offer services such as insurance, and carry out activities such as surface mining.

More broadly, those states that have brought in such requirements have so far done so only at a national rather than a regional level. This means local producers miss out on economies of scale that could come with wider integration. However, this is a dynamic area and countries such as Zambia and the DRC are already moving away from insular industrialisation policies to push for more regionalised value chains, especially in cell manufacturing and automotive assembly.

A win-win model: Foreign investments in African CRMs

African countries’ growing use of local content obligations is already shaping investment patterns and delivering wins for them. Largely thanks to these policies, this investment is producing offshoots of local value-added mineral production and wider economic benefits.

The dominant external investor in African mining is China. Boosted by earlier interventions such as the Belt and Road Initiative, Chinese-backed companies have acquired lithium mines in Zimbabwe and the DRC, and built processing plants to create chemical-grade downstream products. There are variations in how countries have shaped Chinese investment, however. For example, in Zimbabwe beneficiation requirements have encouraged more sustainable, value-added industrial growth largely through Chinese investments. After a 2022 law which banned the export of raw lithium, Chinese mining firm Shengxiang Investments announced in July 2024 that it was nearing the completion of a $40m lithium processing facility near the country’s capital capable of producing 2,500 tonnes a day. The plant is expected to employ more than 200 local people. Associated new infrastructure projects, such as roads, are also under way.

Thanks to this policy, this could be just the beginning for Zimbabwe’s value-added CRM production. This year, four lithium mining companies have submitted plans to Zimbabwe’s government to produce battery-grade lithium in the country. This includes a $310m investment by a consortium of British and Chinese investors to construct a 3m-tonne-a-year lithium processing plant and a $300m spodumene processing plant at the Bikita Lithium Mine owned by the Sinomine Resource Group.

Local obligations are guiding investments in other African countries down a similar path towards more localised value-added production. Planned lithium ore construction plants include the Atlantic Lithium/Ewoyaa Project led by Australian and American investors in Ghana, the Karibib Lithium Project in Namibia led by an Australian company, Lepidico, and the Omaruru Lithium Project also in Namibia, among others. Lepidico is reported to be raising $50m to redevelop two historical lithium mines and build a processing facility designed to produce high-grade concentrates in Namibia. In Gabon, which is the world’s second-largest manganese producer, a $400m manganese smelter has been operational since 2015. This has helped develop a local processing industry, with investors looking to extend value addition to the country’s vast iron ore deposits. Private sector investors now want to build a new 80,000-tonne-a-year battery-grade ferro manganese and silico manganese plant. The Ghanaian government likewise plans to partner with a Chinese company to build a new $450m manganese refinery to add value to manganese, which it has been exporting in raw form since 1916. The refinery is expected to create 400 local jobs and is a significant step towards industrialising parts of Ghana’s economy.

For their part, Gulf players – with the United Arab Emirates (UAE) leading the charge – have also increased their investments in African CRM sectors. Much of these, however, have been signed with existing mines, which existing contractual obligations safeguard from the imposition of local content obligations. In July 2023, the UAE signed a 25-year $1.9 billion deal with the DRC to develop four mines. Likewise, Saudi Arabia’s state-owned mining company, Maaden, with support from the Saudi Public Investment Fund, has expressed interest in acquiring existing mining concessions in Burundi, the DRC, and Tanzania by purchasing minority stakes in projects. Through the newly established joint venture, Manara Minerals, another Saudi state-backed vehicle, is looking to secure stakes in Zambia’s copper mines and other countries. These investments are yet to add value to local African economies, but any future deals with new mines would need to meet stricter requirements. With so much sunken cost, the Gulf countries are unlikely to pull away now but – like others – will also fall in line and comply with local obligations.

The era of extractive investment models in Africa is coming to an end. Thanks to the continent’s changing regulatory environment, global players are finding it ever harder to simply buy a mine, ignore local labour and resources, and export the minerals for offshore processing. Global players are quickly realising this old model must change. Indeed, the strength of the local content approach is that it can benefit investors by creating a more efficient value chain. This in turn allows them access to cost-competitive beneficiated CRM products which already have value added. In return, the partner country benefits from job creation and upskilling, technology transfer, and business development.

For African governments, such investment is precisely what they need to industrialise, regardless of whether the partners are American, Australian, British, Chinese, or from the Gulf. Just as the EU’s green transition enters a new, critical phase, and with the bloc attempting to address overreliance on China, it cannot afford to be left in the dust in the race to invest.

The state of play: EU-Africa mineral partnerships

Since 2020, the EU has signed agreements with numerous African states to secure access to CRMs under multilateral initiatives. Aspects of the bloc’s Global Gateway initiative, for example, aim to “enable African countries to integrate their raw materials and resources into sustainable global value chains” by 2030.

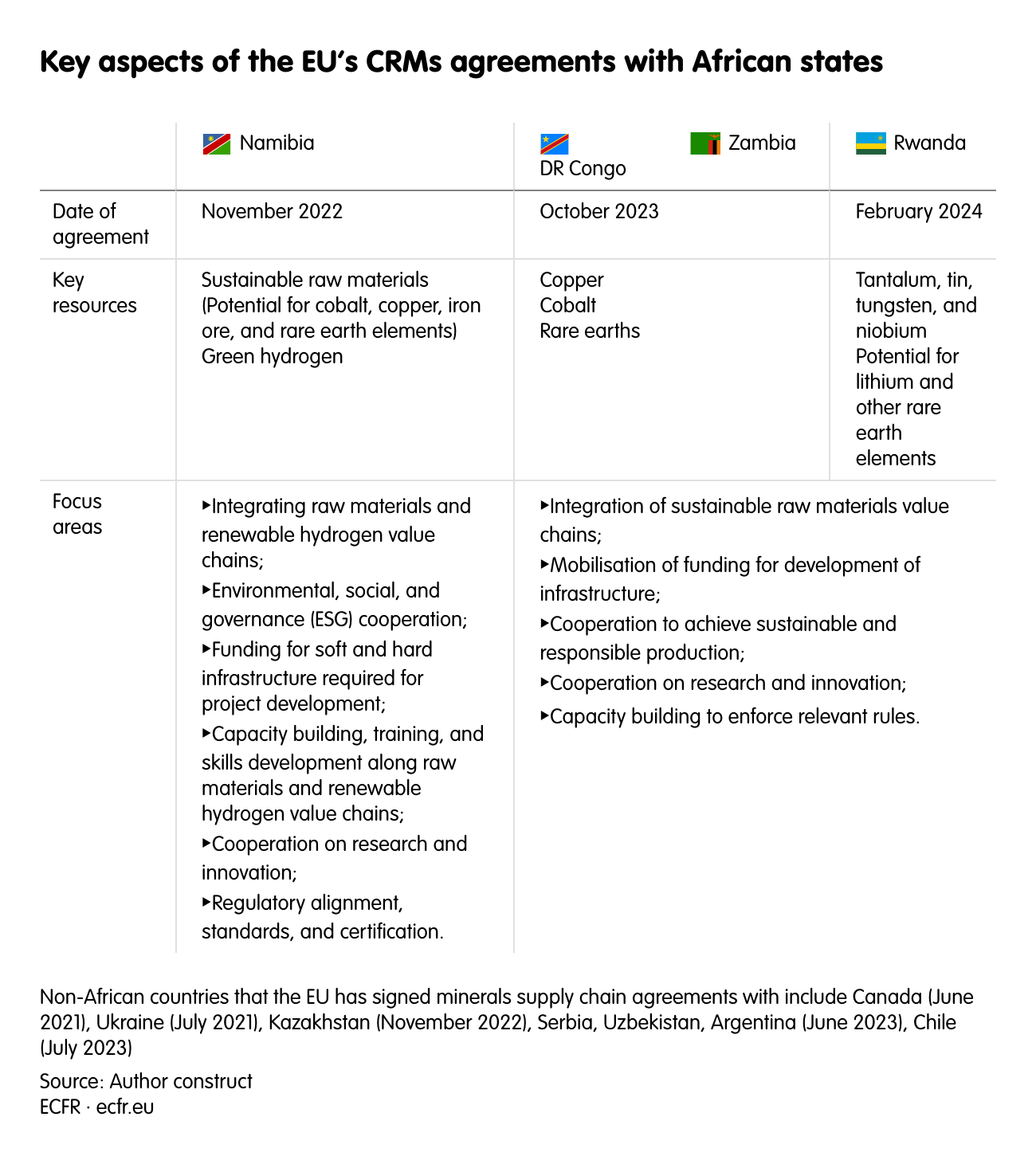

To make this a reality, the EU has signed bilateral partnerships with resource-rich African countries to promote private sector investment in national and regional raw material value chains, including adding value locally. Since late 2022, the EU has signed memorandums of understanding on the supply of CRMs with the DRC, Namibia, Rwanda, and Zambia. These agreements are based on integrating raw material value chains, mobilising funding for development and infrastructure, cooperating on sustainable production, and capacity building, research, and skills training to support these aims./emb

Such renewed engagements in EU-Africa relations have also taken shape through initiatives such as the US- and EU-led trilateral agreement with Angola, the DRC, and Zambia on the Lobito Corridor. This project aims to construct a railway line to connect southern DRC and north-western Zambia to regional and global markets using the Port of Lobito in Angola.

While such progress is commendable, it retains a strong flavour of taking materials out of the ground and sending them out of the country with little opportunity for local economies to benefit more deeply. Such EU investments overlook opportunities to boost production efficiency and scale, strengthen local skills, encourage innovation, and build up local enterprises. To realise African aims of industrialisation and Europe’s need for a resilient CRM supply chain in a cost-competitive and sustainable way, EU policymakers should consider the following recommendations when complying with local content obligations.

The best of both worlds: Making local content rules work for the EU and Africa

Encouraging the regionalisation of local content obligations

The challenge: African countries and organisations have issued renewed calls for a more regional approach to CRM value-addition. The prize would be greater economies of scale and scope. While regional integration is an oft-discussed topic among African states, they often do not collaborate as much as they could. Key obstacles include geographical constraints and the influence of colonialism on intra-African trade and economic relationships. This lack of regionalisation makes it harder for industries to become more competitive and boost firm- and sector-level productivity over the medium to long term. Studies show that regional integration can help improve resource-driven diversification in Africa through cross-border mining transport as well as boost demand for services and goods that feed into that value chain. Deeper integration of regional markets achieved by eliminating non-tariff barriers can also reduce trade and operating costs. For the consumer, this would also mean more cost-competitive CRM supply chains.

The solution: Regionalisation can be achieved by harmonising local content requirements, as seen in the partnership between Zambia and the DRC, which have collaborated to develop battery precursors. Given that many African countries are also members of regional trading blocs – such as the African Continental Free Trade Area, Common Market for Eastern and Southern Africa (COMESA), Southern African Development Community, and East African Community – cross-regional CRM projects can be easily assessed by regional communities for commercial viability in terms of how they drive regional development. For example, nationally imposed quantitative requirements on firms in the form of legally binding targets, such as the number of local staff to be employed, the number of contracts awarded to local suppliers, or the share of spending on local procurement, could give way to regional quantitative requirements. Investors, be they European or otherwise, would then be met with more streamlined regional local content requirements rather than siloed national ones.

To progress this, the European Commission could deepen diplomatic efforts to request more cooperation among these countries. It should emphasise this as a win-win strategy for Africans and Europeans. The commission and individual EU countries could use targeted technical assistance programmes in partnership with regional trading blocs and other agencies to push for the regionalisation of local content obligations.

However, Europeans must recognise that not all African countries are likely to embrace this sort of proposal. Regional local content requires strong cooperation and coordination among all parties involved, which can be challenging in a multi-country context. Some countries may prefer to go it alone. When advocating such an approach, therefore, Europeans can turn to COMESA’s regional local content policy guidelines, which serve as a useful framework for enhancing regional benefits from industrialisation. These are anchored in six principles: domestic capabilities and competencies; creating a level playing field for local citizens’ participation; maximising economic benefits to citizens; improving technological capacity at regional and national levels; mitigation and management of social and political risks; and regional and international legal frameworks. For example, under domestic capabilities and competencies, European investors could give priority to the purchase of local products and services when they are competitive in terms of price, quality, and availability.

Supporting capacity building and education

The challenge: A strong aspect of local content policies is the development of skills in mining, processing, and manufacturing. But in many African countries, the prevalence of low-skilled workers and lack of qualifications in the mining sector is a disincentive to value-added investments and local recruitment. Producers often feel forced to recruit expensive foreign workers; in an annual survey of mining companies in 2022, three-quarters of investors cited the lack of locally available skills as a barrier to investment in the DRC.

In many countries in Africa, a skills base exists for older industries related to mining and processing activities, such as engineering technicians, electricians, and geologists. (Mining companies usually provide training and technical upskilling programmes for workers as part of broader strategies to develop the next generation of skilled miners and engineers to take over more skilled and technical positions.) However, broadly speaking, the continent lacks the highly skilled workers required for new value-chain industries, such as component manufacturing using base metals. Building a precursor cell or battery manufacturing plant requires skills and competencies in chemistry, material sciences, mechanical engineering, and electrical engineering. Similarly, the African Green Minerals Development Strategy identifies that electric vehicle assembly requires professionals in engineering, information and communications technology, and technicians and associate professionals such as robotics engineering technicians and motor vehicle engine testers.

The solution: While some sector-specific skills in areas such as mechanical and electrical engineering are available in the labour force in Africa, investors are failing to deliver sufficient continuous on-the-job training. With this in mind, European private sector investors in African mining and related value chain industries could commit to a minimum annual spend on science, technology, engineering, and mathematics upskilling in African states. They should do this in partnership with local university departments and institutes to provide skills development programmes, including technical and vocational education and training. EU policymakers could provide grants or subsidies to EU private sector mining companies investing in African science, technology, engineering, and mathematics education and innovation. They could further distinguish their offer by proposing the establishment of mining research centres.

In its partnerships with African countries, the EU could also provide seed funding to develop the human capital and technological capacity to integrate African countries into global value chains, especially for manufacturing new technologies. It can do this by creating new training centres that better align certifications and standards such as the Consolidated Mining Standard Initiative. The EU and African governments could jointly fund this. Such an approach would align with the Africa Mining Vision and African Green Minerals Development Strategy and would improve Europe’s bargaining power in negotiations with African partners. From a competition perspective, EU support in these fields would contribute to improving the overall investment environment. It would ensure that there are enough high-skilled workers with the requisite qualifications to support the booming mining industry, for both European and non-European companies.

Promoting technology transfer and innovation

The challenge: Current investments in technology transfer and digital innovation within the mining industry, as measured by global patents, are primarily concentrated in Western countries like Australia, Belgium, France, South Korea, Sweden, and Switzerland. These countries benefit from the presence of mining equipment, technology, and services (METS) companies. These METS firms produce services for the mining sector, such as automation and equipment integration, interoperability platforms, and data enablement via Internet of Things technology. Even within Africa, evidence shows that most general patents are filed from European states, the US, and other high-income countries.

The solution: EU-Africa mining agreements should articulate clear channels through which they would encourage joint research and development between EU and African institutions. The shared aim should be to innovate in mining technologies and practices and promote technology transfer that helps to ensure environmentally sustainable mining. A good example of this is the Centre of Excellence for Advanced Battery Research (CAEB), which launched in April 2022 at the University of Lubumbashi in the DRC. The CAEB seeks to create the skills and competencies as well as the innovation needed for Africa’s nascent battery and renewable energy value chain. A core component of its work is fostering a pipeline of innovative technologies, generating patents and commercialising them. The venture could serve as a useful starting point for similar, larger-scale efforts to boost African innovation.

Developing local businesses and joint ventures

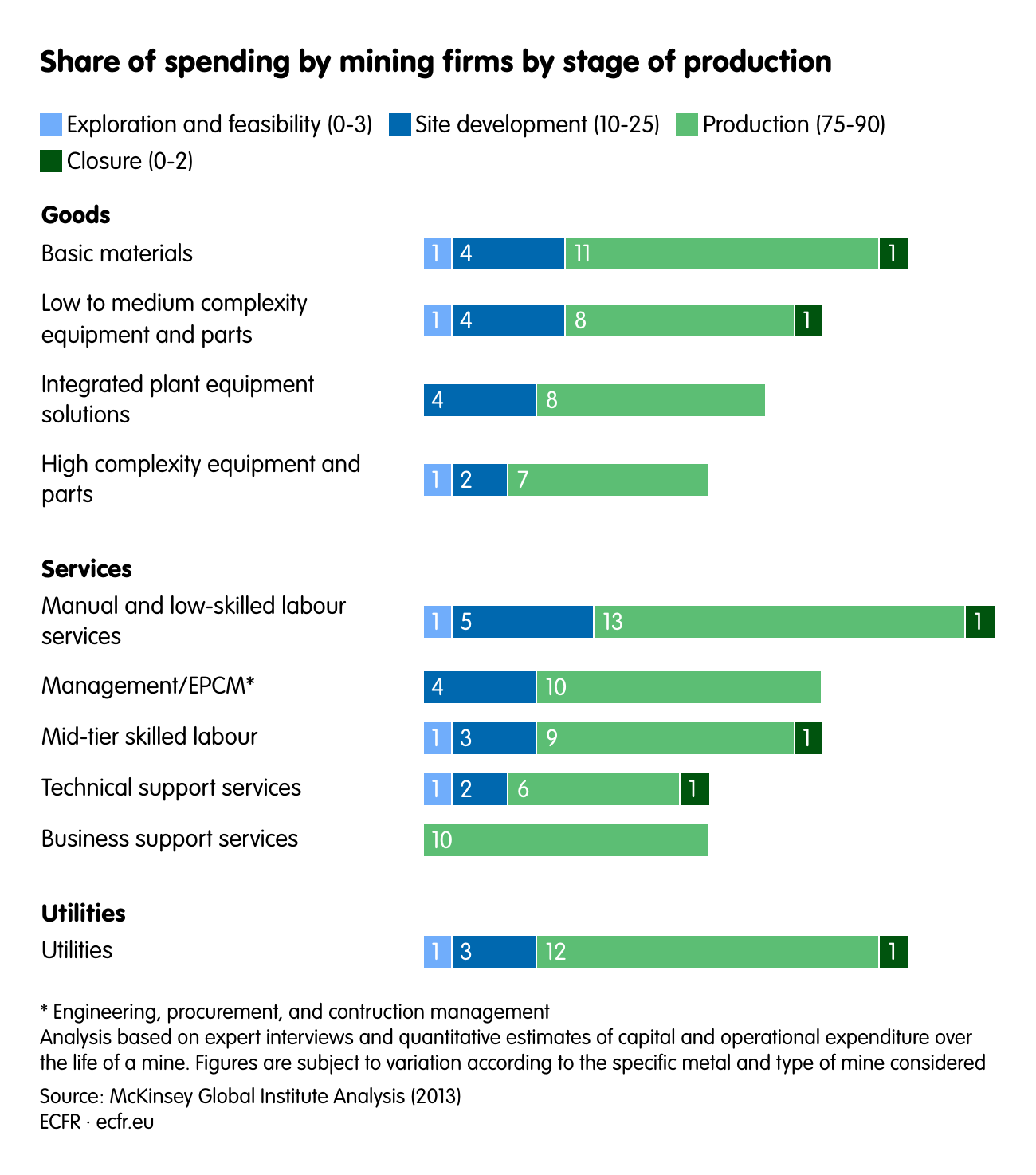

The challenge: Available data show that 75-90 per cent of mining spending, comprising both goods and services, takes place in the production stage. The remaining costs are spread between exploration and feasibility, site development, and mine closure or abandonment. Given that most mining companies’ money ends up in goods and services, African local content obligations require that these spends should be local rather than go abroad. This applies also to European-funded mining ventures on the continent. This is therefore the area in which Europeans can most make a difference for local economies.

The solution: Enhanced dialogue and collaboration between the EU, African governments, and mining companies could boost local content initiatives, especially SME development. Indeed, evidence shows that enterprise development for SMEs and joint ventures can help local companies and communities play a full part in supply chain opportunities, thereby fostering inclusive economic growth and the creation of jobs. Enterprise development strategies with funding from EU institutions and EU private sector programmes could include providing targeted training for small and medium enterprises on access to markets and competitiveness, obtaining financing, and other business development services. EU-backed mining and value-chain projects, like those in the AfricaMaVal project, need to integrate local procurement strategies effectively. By doing so, they can help grow local businesses, enhance the quality and efficiency of supply chains, and establish themselves as trustworthy partners in the region.

Making the investment

The challenge: For the EU to reap the huge long-term benefits of access to a stronger, sustainable CRM supply chain in Africa, it must first commit to funding the recommendations outlined in this paper. Recent estimates suggest that sub-Saharan Africa received just 13 per cent of the new metal and mineral mining operations announced as part of foreign direct investments between 2016 and 2022. Of this, 73 per cent went towards extraction while only 26 per cent went towards processing and manufacturing. African governments want to change and welcome partners that will help them do so, especially on processing and manufacturing.

Europe’s geopolitical competitors, such as China and the Gulf states, use multiple entry points to enter CRM value chains. They are leveraging their sovereign wealth funds and other state-backed vehicles and policy instruments to support mining joint ventures, logistics, and processing facilities in Africa and gain a supply chain advantage. For example, China has promised $1 billion rehabilitation of the old 1,860-kilometre Zambia-Tanzania rail line as an alternative route to market for CRMs, similar to the EU’s plan for the Lobito Corridor.

The solution: The advantages of this policy brief’s recommendations should be realised by securing more European foreign direct investment into Africa’s mining sector and related value chains. In other words, European public and private sector institutions active in actual mining and value chain projects should invest through the EU’s existing partnership agreements with African countries, rather than have the EU rely on related infrastructure like the Lobito Corridor to do all the heavy lifting. The European Investment Bank, German development bank KfW, and other national development banks would be well placed to do this.

Why Europe must cooperate with African countries on local content and beneficiation

For many resource-rich African countries, the old extractivist model of allowing the export of raw mineral ores adds very little to their economies. African governments are taking decisive steps to shift this dynamic. They are implementing local content obligations designed to boost industrialisation and create broader economic benefits. But these obligations are not just a requirement; they are an opportunity for any external partner wishing to engage in Africa’s burgeoning CRM sector. This shift is forcing both traditional players and new entrants to rethink their approach.

For European actors, the message is clear: complying with local content regulations is non-negotiable if they want access to Africa’s CRMs. The strategic benefits of embracing local content are twofold for Europe. Firstly, it presents an opportunity to build a more sustainable and resilient supply chain by establishing African states (and, potentially, regional groups of states) as genuine, long-term partners in the global CRM value chain. Secondly, European companies that engage in value-added production and localisation within Africa’s CRM sector will gain significant cost-competitiveness. This move towards inclusivity and local capacity building will not only secure more stable and competitive access to critical resources – it will also position Europe as a key player in Africa’s industrial transformation. In this evolving landscape, cooperation on local content could be the key to unlocking greater shared prosperity for both Africa and Europe.

About the author

Theophilus ‘Theo’ Acheampong is a visiting fellow with the Africa programme at the European Council on Foreign Relations, where he researches Africa’s role in the global energy transition amid increasing geopolitical competition. Acheampong is an economist and risk analyst with over 15 years of experience working on natural resource governance and public financial management issues. He is an associate lecturer at the Centre for Energy, Petroleum, and Mineral Law and Policy, University of Dundee, United Kingdom and an associate lecturer and honorary research fellow at the Aberdeen Centre for Research in Energy Economics and Finance, University of Aberdeen, UK.

Acknowledgments

I am grateful to Julien Barnes-Dacey, programme director of the European Council on Foreign Relations’ Middle East and North Africa programme and acting director of ECFR’s Africa programme; Maddalena Procopio, ECFR senior policy fellow; Ludivine Wouters, ECFR visiting fellow; and Sarah Logan, ECFR visiting fellow, for helpful comments and great discussions on this paper. I would also like to thank Portia Kentish and Adam Harrison for editing the paper.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.

Source link