Summary

- EU climate action faces opposition from a strengthened populist presence in the European Parliament and in some member states. But the energy transition remains a pragmatic political choice that can help counter some of the very concerns that underpin this “greenlash”.

- The EU and its member states have already expanded their use of renewables, improved their energy efficiency, and grown in the field of clean technology. They now need to protect and build on these successes, particularly in clean technology.

- For the public to feel the economic, energy security, and environmental benefits of the energy transition, the EU and its member states will have to overcome myriad political, investment, and technological obstacles.

- To rise to the challenge, the EU and its member states need to go beyond “green” in their communications strategies. They should also aim to meet their climate goals by implementing existing legislation, while deftly prioritising their funding and their action.

What a difference five years makes

In 2019, Ursula von der Leyen began her first mandate as European Commission president during a period of remarkable public and political support for climate action. Climate change had topped many EU citizens’ lists of concerns that year, which had contributed to a strong showing for the Greens in the European Parliament election (the “green wave”). It was in that context that von der Leyen launched the European Green Deal – a sweeping set of policy initiatives that aimed to transform Europe into the world’s first carbon-neutral continent by 2050.

But the climate crisis has since been joined by more overlapping crises: the covid-19 pandemic, Russia’s war in Ukraine, the war in Gaza and its fallout across the Middle East. This “polycrisis” has pulled the attention of policymakers and public alike in multiple directions. It has also contributed to increased public concern about energy security, high levels of inflation across the bloc, and the corresponding rise in the cost of living.

The European Green Deal itself has become a target for some of these concerns. The agricultural protests that preceded the 2024 European Parliament election, for instance, sparked because farmers feared the EU’s environmental legislation would increase their production costs. These protests were met with understanding and public support in many EU member states. They also drew interest from populist leaders, who saw an opportunity to further their own cause on the back of the farmers’ grievances. Populist parties doubled down on opposition to “green ideology” as a culture-war weapon in the run up to the European Parliament election, helping them achieve historic gains.

Von der Leyen’s second mandate will therefore begin on less consensual ground regarding climate action (ground yet again scorched by a summer of extreme heat across Europe and inundated by floods). Talk of the green wave of 2019 has been replaced with discussions on how to counter the “greenlash”, and how opposition to the European Green Deal could affect the European Union’s and member states’ capacity for climate action.

Nevertheless, von der Leyen has emphasised her continued support for the European Green Deal, and has framed the energy transition as a pragmatic way to strengthen the EU’s competitiveness and energy security. She is right to do so. Continuing to pursue a comprehensive energy transition is a pragmatic political choice. But the EU and its member states will have to find ways to translate von der Leyen’s optimistic statements into actions in today’s more fractious (geo)political environment.

This policy brief aims to guide them in this process. First, it makes the case for the energy transition as a pragmatic political choice and examines the EU’s and member states’ key successes so far. The brief then analyses the challenges that lie ahead for the EU and its member states in continuing to implement the energy transition. Finally, it sets out how the EU and its member states can overcome some of these challenges – and use progress on the energy transition to fight populist narratives of the European Green Deal as an expensive ideological project that impacts on people’s quality of life and their livelihoods.

Green wave to greenlash

The populist argument frames the European Green Deal as an ideologically (“green for the sake of green”) motivated set of measures, invented in Brussels, and disconnected from the economic and social realities in member states. But there remains broad public support for the EU’s goal of achieving net-zero carbon emissions by 2050. And, in most EU member states, people still view the fight against climate change as an important area of public policy. One March 2024 Euronews-Ipsos poll of 18 EU countries found that 52 per cent of respondents considered the fight against climate change a priority.

However, the cost of living was the greatest concern for citizens across the EU27 in 2023. Despite the EU’s progress in renewable energy, energy efficiency, and carbon reduction, people in many countries see these efforts as adding to their already significant economic burdens. This includes some farmers, whose protests before the European Parliament election had a significant impact on narratives of a “greenlash”.

The farmers’ grievances stemmed from new EU environmental standards for the development of the agriculture sector, notably their perceived impact on production costs and competitiveness. Of particular concern were new regulations to reduce the use of pesticides in EU countries by 50 per cent by 2030, the use of fertilisers by at least 20 per cent, and the sale of antimicrobials by 50 per cent. The European Commission backed away from some of these proposals in early 2024. But this did not temper the farming community’s criticism of the European Green Deal – or populist efforts to ride on its coat-tails.

Yet, it is farmers who are likely to be among the most affected by climate change. Intensified seasonal weather patterns are disrupting agricultural cycles and changing rainfall levels; extreme weather events such as heatwaves, droughts, storms, and floods are bringing significant problems for crops and animal husbandry. Implementing solutions to reduce emissions, including energy transition measures, will have a long-term positive impact on the sector.

Other citizens too have expressed concerns about the costs and burdens of implementing some aspects of the European Green Deal. Some drivers, for instance, oppose the EU’s ban on the sales of new combustion engine cars from 2035. Plans to expand green infrastructure such as lithium mines and wind farms also face local opposition, with populists in some countries repurposing this to critique “elitism” in climate policies.

The focus of the greenlash varies across the bloc: northern Europeans tend to view climate policies as infringing on their personal freedoms; southern Europeans are angry about inadequate responses to climate-related disasters; while eastern Europeans are more concerned about the economic impact of green policies, viewing the EU as a “green bully”.

This, combined with geopolitical instability and increased great power competition, has led some European politicians to view the EU’s climate goals as risks that could not only lose them votes but also undermine the bloc’s economic competitiveness and strategic autonomy. What the EU and its member states have to avoid is a creeping prioritisation of economic growth over environmental regulations, which could slow down the implementation of European Green Deal and provoke a shift towards protectionist energy policies. However, the nature of the public opposition to some areas of climate action suggests the EU does not need to back down on its plans for the energy transition. Policymakers should instead view the transition as an opportunity to respond to people’s economic concerns and increase the EU’s energy sovereignty at a time of great uncertainty.

Transition to prosperity and security

Economy

First, the energy transition can bring long-term, tangible economic benefits to the EU, its member states, and their citizens. This is the case for national budgets, the competitiveness of businesses, and the cost of living.

Put simply, fossil fuels are expensive. And the EU’s bill has surged in the years since the covid-19 pandemic and Russia’s all-out invasion of Ukraine. The bloc’s energy import costs reached €604bn in 2022 (rising from a pandemic-distorted low of €163bn in 2021). Between 2015 and 2021, subsidies for fossil fuels in the EU held steady at around €56bn annually (adjusted to 2022 prices), rising to €123bn in 2022. These increases are due to high energy costs during the post-covid recovery and the EU’s rapid and therefore costly diversification away from Russian raw materials, particularly gas.

Globally, it costs around $7trn per year to subsidise the current share of fossil fuels in the economy. According to estimates by the International Energy Agency (IEA), investment in renewable energy sources could lead to significant savings. The IEA looked at both capital costs and operational costs and found that the energy transition would save the world’s economies $12trn by 2050, compared to business as usual with fossil fuels. While the initial outlays may be higher, for instance to upgrade electricity grids and construct wind farms, the long-term savings compared to buying fossil fuels significantly exceed the costs.

The energy transition will also reduce energy prices in the EU in the long term. Electricity produced from most renewable energy sources is now cheaper than that produced from most fossil fuels. Broadly speaking, gas is the cheapest conventional source of energy: gas-fired power plants clock in at $45 to $108 per 1 megawatt hour (MWh), with those gas plants that generate power only at peak times costing $110 to $228 per 1MWh. Coal-generated and nuclear energy are often considerably more expensive. Among renewables, onshore wind enjoys the lowest production costs ($27 to $73 per 1MWh). The production cost of offshore wind ranges between $74 and $139 per 1 MWh. In terms of photovoltaics, energy generated from rooftop installations costs the most (as much as $284 per 1MWh), but commercial and industrial photovoltaics are cheaper, with costs ranging from $54 to $191 per 1MWh.

Crucially, the cost of producing electricity from solar photovoltaic technology is now 82 per cent lower than it was in 2010; for onshore wind 39 per cent lower; and for offshore wind 29 per cent lower. This is because technological advances have reduced the cost of building installations such as solar and wind farms. According to IRENA, n 2022 the renewable power deployed globally since 2000 saved an estimated $521bn in fuel costs in the electricity sector. In the future, the costs of offshore wind and photovoltaics are likely to decrease further, joining onshore wind in outcompeting not only coal and nuclear, but also gas.

Energy security

Second, the energy transition strengthens countries’ energy security or energy sovereignty, another major concern of politicians and public alike.

Russia’s all-out invasion of Ukraine demonstrated the risks of depending on single fossil-fuel suppliers. From spring 2022 onwards, Russia began to reduce or cut off gas supplies to its European customers in an attempt to blackmail them into changing their policies on Ukraine. Europeans, in turn, had to quickly find alternative suppliers to ensure the stability of their electricity systems and gas-using industries.

Renewable energy sources are therefore of practical importance for energy security – and investments in renewables and the expansion of their installed capacity have mitigated the effects of the energy crisis since 2021. A good example among EU countries is Denmark, which already obtains about half of its electricity from domestic renewable sources. This means it is less dependent on external suppliers and more insulated against geopolitical shocks.

Investment in energy grids is crucial for the development of renewable potential. This is because the extension of networks (especially distribution networks) is necessary for the connection of new renewable installations, in particular photovoltaic installations. But investment in grids can also strengthen energy security in the event of sabotage or external aggression. Ukraine’s energy grid demonstrates this: the country’s decentralised electricity system and its connection to the EU grid (Ukraine’s and Moldova’s electricity grids were synchronised with the EU grid in March 2022), allowed Ukraine to survive early Russian attacks on its energy infrastructure. This proved especially valuable during the first winter after the invasion. Continued Russian attacks on Ukraine’s energy infrastructure have led to a massive energy crisis, but the decentralised nature of this infrastructure (including renewables installations) means Ukrainians have been assured of at least a few hours of electricity each day.

These are just a few examples of the benefits the EU and its member states have gained and will gain from the pragmatic choice of continuing the energy transition.

The bright spots of the EU’s energy transition

The implementation of the European Green Deal is already under way across the EU, and its impact has been far from “disastrous” (as some populist narratives would have it). One key driver of the successes so far is that Brussels has broadly “Europeanised” the energy transition agenda. That means the transition has become the focus of energy policy in all EU countries – notwithstanding differences in opinion between member states on the pace of the transition and their ambitions in terms of targets, as well as levels of political interest. It is therefore crucial for the EU and member states to harness this momentum, protecting and building on their successes to date.

The growth of the renewables sector

The first cause for celebration is the growth in the EU’s renewables sector. The bloc has significantly increased not only its renewable potential in terms of installed capacity, but also the share of renewables in its electricity production. Between 2014 and 2023 the EU increased its renewable generation capacity from 352 gigawatts (GW) to almost 642GW. The increase in solar power capacity is particularly impressive, and the sector set a record for commissioning in 2023 (55.9GW which represents a 40 per cent year-on-year increase). Consequently, the EU’s total generation capacity for solar power rose to nearly 260GW in 2023. This slightly surpasses the total installed capacity from all energy sources in Germany (240GW).

In 2008, the EU set a target for a 20 per cent share of renewables in the bloc’s energy mix by 2020, which turned out to be realistic – in fact, by 2020 it had reached 22 per cent. All EU member states achieved their individual renewables targets for 2020 except France, largely because the country has a large share of nuclear power in its energy mix. Moreover, in 2023 the share of renewables in the EU’s electricity production exceeded 40 per cent for the first time (44 per cent), and wind produced more electricity than gas in 2023 for the first time in the history of the bloc.

The recent boom in renewables development, particularly in photovoltaics, is to some degree a consequence of the EU’s and member states’ climate strategies, including subsidies to incentivise the use of solar panels. But external factors also play their part: geopolitical turbulence is increasing European interest in energy projects that reduce risks to the stability of raw material supplies (in particular, the bloc’s high level of dependence on China). And, as discussed, increased domestic renewable potential is one way to strengthen such energy sovereignty.

But renewables have also proven an increasingly appealing choice for companies and consumers, irrespective of government strategy. Renewable technologies offer new opportunities for individuals to become energy producers themselves and play an active role in the energy transition. This can involve households and businesses installing solar photovoltaic panels on their roofs or citizens forming energy cooperatives to establish district heating networks. Such active involvement in the energy system is known as “prosumption”. In this model, individuals are both producers and consumers (known as “prosumers”) and reap economic benefits from it. The number of energy prosumers in the EU has increased significantly over the past few years.

This is mainly because technological progress has significantly reduced the cost of renewable technologies. Solar panels, for instance, have become much cheaper, in part because smaller amounts of critical raw materials (CRMs) are needed to produce their batteries. Electric vehicles have also become much cheaper as new battery designs have cut cobalt demand by half over the past five years. (Cobalt is toxic, highly subject to fluctuations in price, and presents ethical concerns due to mining conditions in the Democratic Republic of the Congo – DRC – where most supplies originate.) Nickel-free batteries now account for around 40 per cent of batteries used in electric cars (in 2019, they accounted for just 7 per cent). By 2040, 50 per cent of the lithium used to make new batteries could be recycled from used lithium batteries.

The EU’s progress on renewables has already contributed to a decrease in its carbon footprint. In 2023 the EU’s carbon emissions reached their lowest level in 60 years. This was thanks in part to a record drop in emissions from the electricity sector (157m tonnes or 19 per cent year on year). But the emissions intensity of the electricity sector also fell in 2023, to down from almost 343 grams of carbon dioxide equivalent (gCO2e) per kilowatt hour a decade ago. This was made possible by the increase in electricity generation from renewables, but also by an increase in the production of relatively low-carbon electricity from nuclear power plants and a reduction in electricity consumption. The EU’s Emissions Trading System (ETS) has also played a role: since its launch in 2005, the scheme has reduced the amount of carbon dioxide generated by the power and industry sectors by 37 per cent. The ETS has also generated more than €152bn since 2013, which most EU countries have invested in the energy transition.

Crucially, this reduction in emissions has been accompanied by a decrease in wholesale energy prices in the EU. One IMF analysis found that, between 2014 and 2021, every 1 per cent increase in the proportion of electricity generated from solar and wind power translated into an 0.6 per cent average drop in wholesale electricity prices in Europe (24 countries, including non-EU Norway, Switzerland, and the United Kingdom). Moreover, the IEA estimates that EU countries saved a total of around €100bn in the period 2021-2023 due to the increase in electricity production from renewables. This is a golden opportunity for the EU and member states to demonstrate to the public how renewables are part of the solution, not only to climate change but also to citizens’ economic concerns.

Clean technology

The growth in the EU’s renewable potential and the prospects for further expansion of this sector are dependent on the development of clean technologies such as wind turbines and solar panels. The EU remains heavily dependent on imports for clean technology and its components, but it has also developed some potential of its own in this field.

The global wind turbine manufacturing market is dominated by ten companies, five of which are based in the EU: Vestas, Siemens Energy, Enercon, Nordex SE, and GE Renewable Energy. This has helped the EU meet both its own needs and become a net exporter of wind technology. Although the EU is a net importer of batteries used in photovoltaics, it has also developed some potential for battery cell manufacturing. As of 2023, the EU had a total battery cell manufacturing capacity of 204 gigawatt hours (GWh), which was just slightly less than the demand of 210GWh for electric vehicles and energy storage systems. This indicates that the EU meets virtually all its current requirements through domestic battery production.

Moreover, some EU countries can boast technological achievements in optimising demand for CRMs in the production of green technology. Spain has been particularly successful in this field, having recently developed its first large-scale cobalt-free lithium-ion battery for electric vehicles. The EU is also a leader in the design and production of smaller ground-source heat pumps (that use geothermal energy) and larger heat pumps that are used for commercial and district heating and cooling systems.

Strengthening international cooperation

Despite the EU’s domestic progress, the development of clean technologies still requires international partnerships and carefully managed interdependencies with third countries. This includes the sourcing of CRMs such as lithium. To date, the EU and its member states have been relatively successful in establishing such partnerships to achieve their energy transition goals. The bloc has concluded political cooperation agreements on CRMs with countries such as Argentina, Brazil, Canada, Chile, Namibia, Kazakhstan, Japan, Morocco, Uruguay, and Zambia.

Crucially, the EU has also opened negotiations with the United States on cooperation in the sphere of CRMs. One of the main goals of this is to promote EU-US supply chains for the CRMs used in manufacturing electric vehicle batteries. Concluding an EU-US Critical Minerals Agreement would grant the EU the same status as US free trade agreement partners under the US Inflation Reduction Act, allowing EU firms to compete equally with US and global competitors in the US market. This agreement could also boost EU production in strategic industrial sectors, ensure the sustainable sourcing of critical raw materials, and support the EU’s goals to scale up manufacturing of carbon-neutral technologies through the Net Zero Industry Act and Critical Raw Materials Act.

Beyond these arrangements, EU member states have also joined alliances to foster international cooperation on critical raw materials. In 2022 the European Commission and some EU countries (Finland, France, Germany, Italy, and Sweden) became members of the Minerals Security Partnership (an alliance of 14 countries and the EU that aims to stimulate public and private investment in responsible global critical minerals supply chains). France Germany and Sweden have also joined the Sustainable Critical Materials Alliance (an association founded by Canada to promote the worldwide adoption of environmentally sustainable, socially inclusive, and responsible practices in mining, processing, and recycling, as well as in critical minerals supply chains). And in 2020, the European Raw Material Alliance was established within the EU itself, focusing on the challenge of ensuring reliable access to sustainable raw materials, advanced materials, and industrial processing expertise.

Partnerships such as these help the EU and member states develop clean technologies, thereby accelerating the energy transition. But they also play an important role in reducing dependence on and de-risking from China, which currently dominates the supply chains of many CRMs. Some of the alliances could also improve cooperation with the global south and compete with growing Chinese and Russian influence in those countries. This all contributes to boosting both the EU’s competitiveness and its energy security.

Improvements in energy efficiency

Beyond renewables and clean technology, the efficient use of energy is crucial to the EU’s energy transition process. Energy efficiency contributes to less demand for electricity and heat, leading to significant savings – in energy and, consequently, money.

The EU and its member states have made good progress in this area. This is the case both for reducing waste in the process of generating electricity (“primary consumption”, which is the total energy used before and after it reaches the consumer) and in the energy consumed by end users, such as households, industry, and agriculture, (“final consumption”). The covid-19 pandemic, which involved drastic reductions in energy consumption associated with numerous lockdowns, helped produce some record numbers. In 2020 the EU’s primary energy consumption hit a low of 1236m tonnes of oil equivalent (Mtoe), exceeding the bloc’s 2020 energy efficiency target by 5.8 per cent. Most EU member states also achieved their individual primary and final energy consumption targets.

But the EU had been on a path to improved energy efficiency well before 2020. Between 2005 and 2020, the EU introduced various energy efficiency policies and regulations, with the most notable being the Energy Efficiency Directive of 2012, which established binding energy-saving targets. The EU also set energy performance standards for buildings, appliances, and vehicles, significantly reducing energy consumption. Additionally, the transition to renewables is further enhancing the EU’s overall energy efficiency, as these technologies are typically more efficient and experience lower energy losses than traditional fossil fuels. Technological innovations played a key role in boosting energy efficiency across sectors, with advances in industrial processes, building materials, and energy-efficient products such as LED lighting leading to significant energy reductions.

Russia’s all-out invasion of Ukraine underlines how EU countries can reduce their demand for fossil fuels in times of crisis, particularly gas. Member states achieved a 19 per cent reduction in natural gas consumption between August 2022 and January 2023, equivalent to 41.5bn cubic metres. This was a result of common rules established in summer 2022, which set a voluntary target to reduce natural gas use by 15 per cent between August 2022 and March 2023, compared to the average consumption over the previous five years.

*

The EU’s achievements so far in the energy transition have thus brought tangible economic, security, and environmental benefits to member states. They have also strengthened the EU’s energy sovereignty. This all provides further backing for the energy transition as a pragmatic political choice – and not a question of “green ideology”.

The challenges ahead for the EU’s energy transition

To build on their successes, the EU and its member states will need to overcome several more challenges in the years ahead. These hinge on the perennial matter of funding, which may become more difficult still as the EU and member states spend more on defence. The EU’s ambitious 2030 targets may also prove hard for member states to achieve, particularly given the increased populist opposition to climate action. Finally, the EU and its member states have work to do regarding their dependencies on third countries, as well as their energy diplomacy more broadly.

The question of funding

The overarching challenge for the EU’s energy transition is the amount of investment that it needs to reap the returns – in terms of economic and environmental benefits and improvements to energy security. The EU has set up a range of institutions and initiatives to provide financial support for the transition. But the resources at their disposal may not be enough to meet all member states’ (unequal) needs.

In the coming years, the EU plans to spend a total of around €600bn on climate-related measures. These funds are carved out in the EU’s multi-year budget for 2021-2027 and in its NextGenerationEU covid-recovery funding for 2021-2026. A significant amount of the €600bn is earmarked for investment in the energy sector. However, for the EU to achieve its transition goals, energy investments will need to reach close to €400bn a year between 2021 and 2030 and as much as €520-575bn a year between 2031 and 2050.

The shortfall is laid bare in the budgets of the instruments through which the EU financially supports the energy transition in its member states, including but not limited to the Modernisation Fund (which aims to support 13 member states to meet their energy targets by helping to modernise energy systems and improve energy efficiency); the Just Transition Fund (which supports countries expected to be the most affected by the transition towards climate-neutrality); and the Social Climate Fund (which provides EU member states with funding to support vulnerable groups affected by the green transition). Moreover, the ability of each member state to fund the transition and take advantage of EU instruments varies significantly – for instance, the European Commission more readily accepts large sums of money to be spent by already rich countries, exacerbating inequalities.

What is more, the EU will have to invest in people to propel the energy transition (using, for instance, the Just Transition Fund and the Social Climate Fund, both of which foresee this need). This applies, for example, to staff working in fields such as the installation of heat pumps or retrofitting district heating. The skills deficit could prove very serious in the years to come: according to forecasts from McKinsey, by 2030 nearly 1 million skilled workers will be needed in the renewables sector, which is three times as many as today.

These investment needs are being exploited by opponents of the European Green Deal, who portray the energy transition as a huge cost rather than a long-term investment that can deliver tangible economic benefits and savings in consumers’ wallets.

The securitisation of the EU’s priorities

The investment challenge may be exacerbated by shifting EU priorities in the face of geopolitical instability. Security and defence are necessarily taking up an increasing amount of policymakers’ attention. The danger is that the upheavals – most notably the threat to European security posed by Russia – push energy transition issues down the list of the EU’s and member states’ priorities (especially if politicians also think climate action may not be the vote-winner it was in the past).

Russia’s war in Ukraine is forcing EU member states, the vast majority of which also belong to NATO, to increase their defence spending. It is very likely that countries on the eastern flank of the EU, faced with an existential threat from Russia, will not only prioritise the security sector as part of their national spending planning, but will also push for the EU to become more active in strengthening defence and security issues as part of its agenda.

In February 2024, for the first time since NATO was established, its European members decided collectively to allocate 2 per cent of their combined GDP to defence spending in 2024. According to the outgoing NATO secretary general, Jens Stoltenberg, European members of the alliance will invest a combined total of $380bn in defence over the course of year. This may end up diverting investment from other areas, including the energy transition.

If Donald Trump wins the US presidential election in November, he may load even more pressure onto European defence spending. But, as my ECFR colleague Camille Grand has argued, even if Trump loses the EU would be well advised to seek more autonomy from the US in terms of defence. This complicates the balancing act the EU and its member states are already performing in the face of multiple urgent and competing priorities.

Difficulties meeting new targets

In the face of investment and security challenges, member states may struggle to meet the EU’s 2030 climate targets. With the 2021 Fit for 55 package (a collection of legislation designed to implement the European Green Deal), the EU had already tightened its 2030 climate targets with the aim of reducing EU greenhouse gas emissions by 55 per cent from 1990 levels by 2030. Some of these targets, for instance for renewables projects and energy efficiency, were tightened further in 2023.

Renewables

As discussed, the EU is making good progress each year in expanding its renewable potential. But the 2030 targets may prove difficult. The revised target is a hefty 42.5 per cent renewables share in final energy consumption by 2030. The bloc is on track to meet the solar aspect of this goal (an increase from nearly 260GW of capacity in 2023 to 600GW by 2030. The problem is wind. While 2024 has been a record year for the EU’s wind generation capacity (16.2GW), the bloc will need 29-33GW of new wind capacity each year to meet the revised target of 425GW by 2030. One reason for the relatively weaker performance of the wind sector is delays in obtaining permits for projects. This issue tends to hit this sector harder than solar due to more stringent regulations, for example, concerning the location of onshore installations.

The EU’s ageing electricity grids may also prevent the renewables sector from meeting its targets. The deteriorating state of Europe’s grids has already slowed the energy transition: ageing grids are inefficient and cannot be connected to new sources of renewable energy, which creates a bottleneck on renewables generation in some member states. Around 40 per cent of the EU’s networks are more than 40 years old, just ten years out from their typical lifespan. These issues affect transmission grids, distribution grids, and the extension of interconnectors between EU countries and between the EU and third countries. Better and expanded energy grids would also improve the EU’s storage potential, which will be essential for the EU to capitalise on the progress it has made in renewables. Analysts and consultancies estimate that each additional 1GW of renewables capacity will require grid investments of between €0.9bn and €3bn, which in total would amount to between €470bn and €1.65trn by 2030. This compares to around €130bn spent on grid expansion across the EU between 2011 and 2020.

Energy efficiency

The EU’s tighter targets for 2030 may be even more challenging in terms of energy efficiency. The new targets include the EU limiting its primary energy consumption to a maximum of 992Mtoe by 2030, compared to the 2020 goal of 1128Mtoe. And, by 2030 the EU’s final energy consumption should not exceed 763Mtoe. This will be difficult considering the EU’s projected final energy consumption for that year is 846Mtoe, and in 2022 the EU exceeded the 2030 target by 23.3 per cent.

One of the most sensitive sectors is buildings, which account for around 40 per cent of the EU’s final energy consumption and 36 per cent of its energy-related greenhouse gas emissions. Currently, almost three-quarters of buildings in the EU are energy inefficient. The EU’s recast energy performance of buildings directive (adopted in 2024 as part of the Fit for 55 package) aims to mobilise member states to accelerate the thermal upgrading of buildings – for instance, through better insulation or double glazing on windows. It also included proposals for the eventual phase-out of gas boilers.

The directive does not impose stringent obligations on member states. But it still triggered a backlash in some countries. This was mainly due to a lack of effective communication from the EU, as well as misinformation from populist politicians. The directive does not, for instance, introduce a top-down obligation to renovate all buildings including private homes (a claim that circulated in some parts of the media). Rather, it introduces a general renovation obligation only for non-residential buildings such as hospitals. It is only when the owner of a house or block of flats decides to carry out a major renovation that they would be obliged to improve its energy performance. Another falsehood that circulated in the media is that gas boilers will be banned from 2040. But the directive only indicates in general terms that member states must endeavour to replace fossil fuel boilers in existing buildings. The manner and timing of this obligation is for the individual member state to decide. These examples illustrate how ambitious targets can (wilfully or otherwise) be misunderstood, potentially hindering progress towards meeting them.

The EU also revised its ETS directive in 2023 and incorporated new measures to boost the bloc’s energy efficiency. The directive includes a new scheme to cover the buildings and car transport sectors (ETS2). But the implementation of these measures could prove challenging, especially in countries where coal and other fossil fuels still dominate in the electricity and heating sectors. The directive stipulates that suppliers of fossil fuels for the sectors covered by the scheme will have to buy emission allowances from 1 January 2027. This will lead to an increase in energy costs for households using fossil fuels (as fuel suppliers will pass on the cost of buying allowances to end users). While the EU has stated that it may delay the implementation of ETS2 one year if oil and gas prices are too high, this could end up kicking the can of higher costs down the road for some consumers (notably in coal-intensive eastern European states – where some of the public already tends to view the EU as a “green bully”). This is because it will take carbon-intensive member states considerably longer to reduce the amount of fossil fuels in their economy than a year.

Intra-EU inequalities in an energy transition race

The EU’s current rate of emissions reduction will not be enough for the bloc to achieve its ambitious climate goals. A report from the EU’s climate advisory board found that, to meet the targets of a 55 per cent reduction in emissions by 2030 and climate neutrality by 2050, the EU would have to double its current rate of emissions reduction.

One key challenge in this regard is the varying pace of the energy transition in different parts of the EU and conflicting opinions among member states on the way forward. The World Economic Forum’s energy transition index, which it compiles based on criteria such as the carbon intensity of the economy, the share of renewables in electricity production, and carbon dioxide emissions per capita, rates some EU countries in the global top ten (Sweden, Denmark, Finland, France, Austria, the Netherlands, and Estonia); while some lag well behind (Poland, Ireland, Belgium, Slovakia, Czech Republic, Bulgaria, Romania, Cyprus, and Malta). High current levels of carbon intensity may make the road to climate neutrality longer for some EU countries (such as the Czech Republic and Poland), while it may be shorter for Scandinavian countries, France, Italy, and Germany. The EU will need to address the inequalities that underpin these differences if it is to ensure the energy transition progresses in all member states and to meet its emissions reduction targets.

Renewables potential is one site of uneven distribution across the EU. Solar energy, for instance, is more extensively deployed in north-western European countries such as the Netherlands, Germany, and Belgium, rather than in traditionally ‘sunny’ southern countries. Nordic nations, including Sweden, Denmark, and Finland, are at the forefront of wind energy deployment. They are also leaders in the installation and use of heat pumps. This is largely due to differences in budgets, energy-strategies, and priorities among EU member states.

Inequalities also apply to the development of electromobility. According to data for 2023, as many as 52 per cent of electric vehicle charging points are concentrated in 10 per cent of EU territory (primarily in Germany, the Netherlands, and France). The Netherlands, for example, boasts more than 70 times as many charging points as Romania. This inequality skews the EU average: only seven member states enjoy more than the mean of 106 charging points per 100,000 inhabitants; in Cyprus, Greece, Poland, and Romania, number of charging points is ten times lower than the EU average.

Energy poverty is also unequally distributed across the EU. According to EU data, in 2022 as many as 42 million people (almost 10 per cent of the bloc’s population) had to reduce their energy consumption to the degree that it affected their health and wellbeing. Bulgaria is the member state most affected by energy poverty. In 2022 more than 20 per cent of Bulgarian households were not able to sufficiently heat their homes, with Cyprus and Greece not far behind (18 per cent in each country). In some member states, however, energy poverty rates are far lower: Finland (1.4 per cent), Luxembourg (2.1 per cent), Slovenia (2.6 per cent), Austria (2.7 per cent), and the Czech Republic (2.9 per cent). Energy poverty results from a combination of three key factors: low incomes, high energy expenses, and inadequate energy efficiency in buildings. The energy transition itself could therefore be part of the solution to energy poverty, but the EU will need to better communicate this to keep all member states on board.

Dependence on third countries for clean technology and CRMs

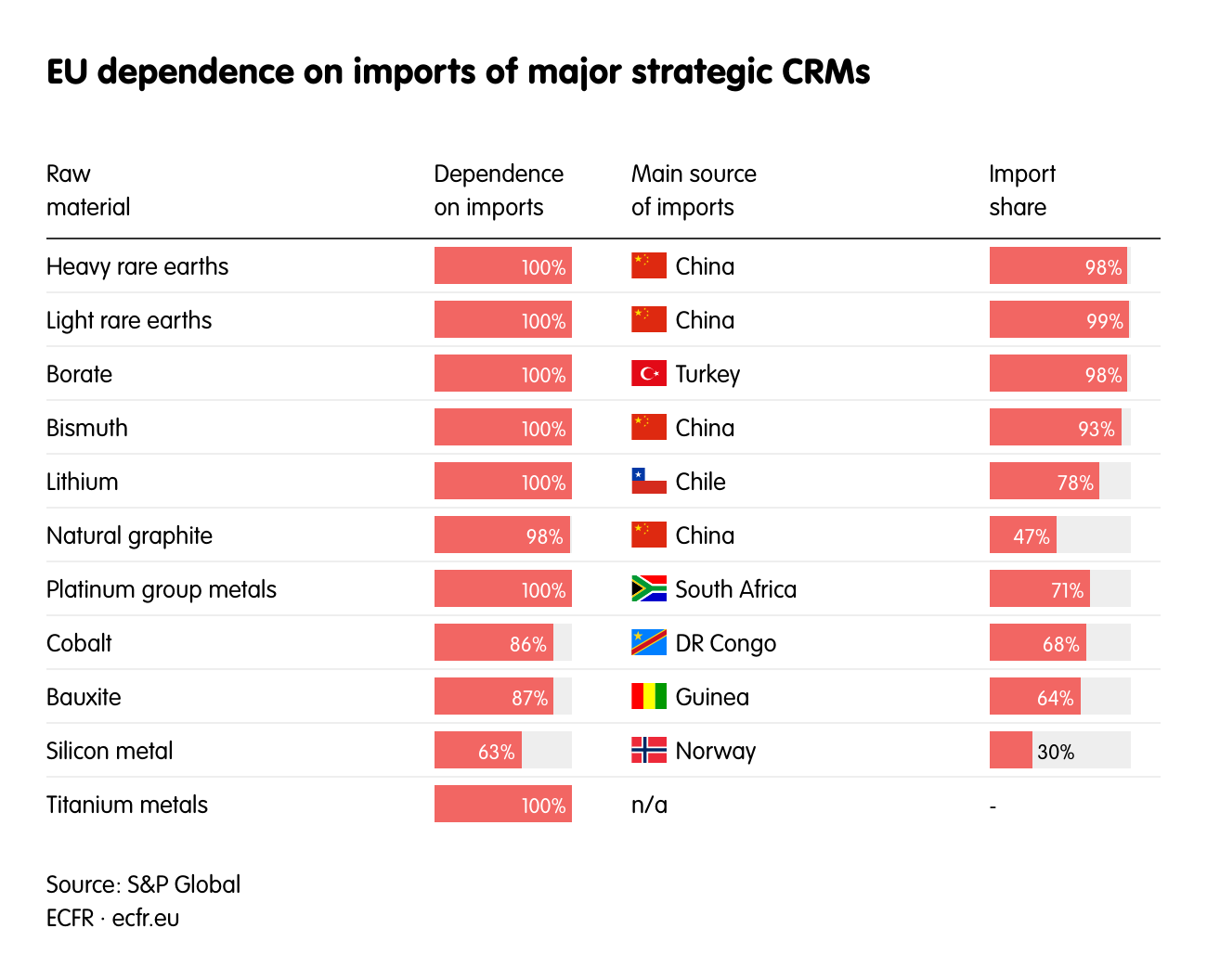

Another major challenge in the energy transition remains the EU’s relatively weak position in clean technologies and CRMs compared to third countries, particularly China.

The EU has sufficient manufacturing capacity to cover most or even all its deployment requirements for technologies such as onshore and offshore wind (within the constraints discussed in the previous section). But in other sectors, particularly solar photovoltaic, the EU still relies heavily on imports.

Chinese-produced solar panels account for more than 95 per cent of the EU’s total imports in this sector. And the EU’s potential in terms of installed battery manufacturing capacity may have increased in recent years, but that growth is incomparable to that of world-leader China. Europe lags behind both China and the US in most venture capital investments for clean technology, with its performance only satisfactory in the realm of charging infrastructure and battery manufacturing. Such a high level of import dependency threatens the development of the producer industry in the EU. It also means that far more jobs in Europe are generated by solar energy in the installation sector than in the manufacturing sector.

One of the most significant challenges of the energy transition is the EU’s heavy reliance on CRMs, particularly those that the EU itself has recognised as strategic in its 2024 Critical Raw Materials Act. The list of raw materials the EU considers critical has steadily expanded, from 14 in 2011 to 34 in 2023, of which the EU has designated 17 also as strategic raw materials. These include light and heavy rare earths for which the bloc depends almost entirely on China for imports.

The EU’s 2030 targets for CRMs are very ambitious. According to the Critical Raw Materials Act, Brussels plans for 10 per cent of its annual consumption of CRMs to be extracted within the EU, 40 per cent processed within the EU, and 25 per cent recycled within the EU by 2030.

EU member states do not have large reserves of these minerals, but the 10 per cent target could be achievable with the necessary investment. Poland, for example, accounts for 1.5 per cent of global copper mining and has some limited nickel resources. New Caledonia (a French overseas territory) accounts for 5.8 per cent of global nickel production. Sweden has relatively significant lithium resources, and in January 2023 the Swedish company LKAB reported finding the largest known deposit of rare earth elements in Europe. Cyprus has copper deposits; Spain has cobalt deposits; and Greenland (a Danish overseas territory) has deposits of cobalt, nickel, and copper, among others. In addition, some non-EU European countries also have some resources of critical raw materials, in particular lithium: Serbia, the UK, and Bosnia and Herzegovina. In this context, it was a promising step for the EU to conclude a memorandum of understanding with Serbia in July 2024 that established a strategic partnership on sustainable raw materials. The EU also accounts for a small share of global processing of CRMs: Finland (cobalt, 11 per cent), Germany and Poland (copper, 2.4 and 2.3 per cent respectively) and Estonia (Neodymium, 1 per cent). It therefore has a long way to go if it wants to process 40 per cent of its annual consumption within the bloc.

Global resources of CRMs are sufficient to fulfil the rest of the EU’s needs. The problem is the rate of extraction, which is not fast enough given the global growth in demand. According to the IEA, global lithium demand could increase up to tenfold by 2050 compared to 2022. A 2021 briefing for the European Parliament projected that Europe will require 18 times more lithium by 2030 and 60 times more by 2050 to satisfy the expected demand for electric vehicles, which primarily rely on lithium-based batteries. From the EU’s point of view, this means having to compete with other raw material importing regions. Meeting this demand will also involve significant capital investment for new mines and refineries in developing countries that boast the largest lithium deposits (Chile, Argentina, and Bolivia). For newly discovered deposits, there is usually a seven-year lag until the start of production.

In addition to the issue of the rate of growth of supply, the EU will also face challenges in diversifying its sources of supply of CRMs. The Critical Raw Materials Act stipulates that by 2030 no more than 65 per cent of the annual consumption of each strategic raw material can come from a single country. Currently, the EU is still dependent on importing individual CRMs from one dominant supplier (China in most cases). Moreover, some of these countries may represent political risks to the EU (China and the DRC).

Addressing these dependencies is not the only international challenge for the EU and its member states in continuing the energy transition. They will also need to reassess the way some member states have conducted their energy diplomacy more broadly, especially in the wake of Russia’s all-out invasion of Ukraine.

Self-interested energy diplomacy from EU member states

EU member states have intensified their energy diplomacy over the past two years, which is a positive development. But some member states have approached these efforts in an overly individualistic way. This creates the risk of stranded assets and costly contractual obligations for fossil fuel supplies beyond 2050. ECFR’s Energy Deals Tracker, which maps the EU’s new energy agreements since February 2022, shows that as many as 45 per cent of the deals concerned cooperation to replace Russian gas with other sources of the same fuel. Of particular concern are the long-term gas contracts European companies concluded with Qatar in autumn 2023 for the supply of liquefied natural gas to the Netherlands, Italy, and France. Indeed, some of the long-term contracts extend beyond 2050, when the EU plans to achieve net zero greenhouse gas emissions.

How the EU can rise to the challenge

The energy transition is a pragmatic political choice that will bring long-term economic and security benefits to the bloc and its citizens. It is also a huge undertaking that will hit many obstacles between now and carbon neutrality in 2050.

To reduce “overwhelm” at the idea of addressing these challenges one by one, the EU and its member states should view their efforts to implement the energy transition as falling under three overlapping principles.

Communicate: the EU should accompany its efforts to overcome the challenges discussed in this paper with comprehensive communication strategies that emphasise the long-term, tangible economic and security benefits of the energy transition for the whole of society.

Prioritise: the vast investment required for the energy transition indicates that the EU needs to prioritise most urgent challenges and the most efficient use of funds. This is especially important for the levelling-out of differences between member states in terms of the pace of the energy transition, but also in the most efficient development of energy infrastructure in Europe.

Finish: the EU and its member states should adopt a “finish what you started” mentality that focuses on meeting existing targets through the implementation of regulations, the effective use of existing instruments, and the aggregation of member states’ capabilities.

Under these broad principles, the EU and its member states should focus on the following recommendations.

Develop communications strategies that go beyond “green”

In cooperation with member state governments, the EU should revamp its overall communication policy on the energy transition. This change should focus on communicating the EU’s proposed and implemented legislative changes in an honest and clear manner. Crucially, the campaigns should emphasise the benefits that ordinary EU citizens will enjoy from the energy transition and the European Green Deal more broadly. It should also take into account the variations in reasons for greenlash in different parts of the EU.

Opponents of the energy transition tend to focus on its short-term costs. The EU and member state governments will therefore need to emphasise that the transition is a long-term investment. This should include clear messaging that a failure to transition away from fossil fuels will mean an increase in the cost of living for citizens in the future. They should not shy away from addressing the trade-offs that will be necessary in the short- and medium-term to place these costs in context and seize control of that narrative.

In terms of energy security, the EU and member states should make better use of their response to the Russian invasion of Ukraine. They could, for instance, produce an information campaign that communicates the weaknesses (and expense) of high import dependency and the importance of renewables for greater self-sufficiency (and, ultimately, lower energy prices). The campaign should highlight the biggest success stories in member states since 2022, namely the EU’s significant reduction in dependence on Russia for gas supplies and the fall in gas consumption over the past two years. This would also show the public that significant change is possible within fairly short timeframes.

Invest in electricity grids and energy efficiency

The effective prioritisation of funding will be crucial for the EU to meet its 2030 targets and accelerate the energy transition. It should focus on those areas which can contribute most to reducing energy prices and ultimately bring economic benefits to citizens, but also to the competitiveness of member states’ economies.

The EU’s most urgent task is therefore the expansion and modernisation of the bloc’s energy grids. This includes both interconnections between member states and the expansion of distribution networks in EU member states. The EU can achieve this by increasing funding for cross-border projects that enhance connectivity and integration of renewable energy sources. In addition, it should streamline regulatory processes to facilitate quicker approvals and encourage public-private partnerships. It will also be crucial for the EU to enhance its support for research and development in smart grid technologies and energy storage solutions. This will help ensure that the EU’s grid can accommodate future demand and contribute to a resilient, low-carbon energy system.

After grids, the EU should direct its investment towards improving energy efficiency while clearly communicating that this means real savings for national budgets and the public. A reduction of 1,200 terawatt hours (TWh) of gas consumption by 2027 would save the EU between €127bn and €318bn (EU gas consumption in 2020 was 3,800TWh). The greatest potential for reduction lies in the electricity sector (500TWh), buildings (480TWh), and industries (220TWh to 410TWh).

The EU and its member states should therefore improve existing EU and national instruments that support the expansion of renewables and building modernisation measures. The implementation of the EU’s energy performance of buildings directive can play a special role in this process. Support from the EU and member states for the thermal modernisation of buildings (especially the least efficient) would help the many households that do not have the resources to fund this themselves. The EU and its member states should also communicate to the public that the installation of heat pumps and the thermal modernisation of buildings will reduce their energy costs. Member state action in this area may even prove to be low hanging fruit since buildings account for 40 per cent of EU energy consumption and around 33 per cent of EU emissions.

Finally, the EU should continue and even increase support (including financial) for energy cooperatives in its member states. There are currently more than 9000 energy communities in the EU, but the potential for expansion in this area is much greater. More cooperatives would bring not only tangible economic benefits, but also foster a sense of participation among the public in the energy transition process.

Accelerate decarbonisation in EU member states with highest emissions

The EU should prioritise supporting member states that have highly carbon-intensive economies to adopt ambitious decarbonisation plans. This is particularly the case for central European countries which, on the one hand, are developing the potential for clean industrial development (Czech Republic and Poland), but which may lose out in the medium term due to their high carbon intensity (ETS costs).

Governments in carbon-intensive member states should ensure their updated national energy and climate plans include ambitious and concrete steps – for example, targets to move away from coal in those countries that are still dependent, and which have not made concrete declarations in this regard. They should accompany this with clear communication of the long-term benefits of decarbonisation, particularly for the competitiveness of domestic industries. Member states should also formulate transparent strategies to support the groups most affected in the short term by the implementation of decarbonisation measures.

Central and eastern European countries should also aim to take better advantage of the funds allocated to them through EU instruments. For example, under the Just Transition Fund as much as 56 per cent of the funds or €19.3bn are earmarked for central and eastern European countries. These countries could some of these funds to strengthen cooperation with one another to speed up the energy transition process. Countries such as Bulgaria and Romania, for example, could join forces to develop joint offshore wind projects along the lines of the alliances emerging in the north in the Baltic Sea Basin.

Focus on meeting 2030 climate targets rather than tightening them

The EU’s 2030 targets present significant challenges. But they are achievable, and the EU has already made progress in that direction. Under the European Climate Law, the commission began negotiations in early 2024 for yet more ambitious targets for 2040 (a 90 per cent reduction in carbon emissions against the 1990 level). But pushing for ever more ambitious targets may discourage member states, ultimately increasing resistance to the energy transition that populist forces can exploit.

The EU should create the conditions for negotiations on some areas of Fit for 55 (for example, the postponement of the dates of entry into force of ETS2 mechanisms for households). These would not affect the bloc’s ability to build on the successes of the energy transition so far. But to ensure progress towards the 2030 goals continues, the EU needs to implement the solutions already contained within the Fit for 55 laws and communicate its successes to the public.

The EU should ensure that it balances its climate goals and the ways it has proposed to reach them with the conditions of member states and the interests of business community. This would involve the EU tailoring its strategies to accommodate the unique economic, social, and environmental contexts of each country while pursuing overarching EU climate objectives. It would also mean ensuring that policies are not only environmentally effective but also economically viable, able to foster innovation and competitiveness without imposing undue burdens on businesses. Inclusiveness is crucial. The EU and member state governments should therefore actively engage civil society in the decision-making process. This would help to ensure that all stakeholders, including marginalised and vulnerable groups, have a voice in shaping and benefiting from the energy transition. By harmonising these elements, the EU can advance its climate goals effectively while promoting fairness and broad-based support for the transition agenda.

Aggregate member states’ energy transition needs and capabilities

The European Commission will play a crucial role in aggregating the needs and capabilities of member states in various areas of the energy transition. To do so, it should use the instruments provided for in legislation already adopted under the Fit for 55 package.

The commission could coordinate member states’ efforts to access clean technology and CRMs through mechanisms such as the Net-Zero Europe Platform and the European Critical Raw Materials Board. (Instruments like these aim to increase the capacity of individual member states to develop clean technologies, as well as achieve synergies in cooperation within the EU and between the EU and third countries.) But member state governments also need to improve their cooperation and coordination with one another. The best outcome would be specialisation within the EU regarding the development of clean technologies and the expansion of the bloc’s manufacturing base. This would all increase the chances of the EU as a whole competing more effectively with China and the US.

The EU and its member states should also coordinate their efforts to implement cooperation agreements already concluded with third countries. In so doing, member states should seek out synergies with each other when implementing these partnerships. One example of such cooperation could be the joint negotiation of contracts not only with suppliers of energy resources such as oil and gas, but also with suppliers of clean technologies or critical raw materials. The coordination of member states’ activities could also include the creation of special committees or working groups by member states. This would help prevent conflicts of interest and promote a harmonised approach to energy challenges.

Conclusion

The energy transition is on the one hand a complex challenge for the EU and its member states, but on the other hand an opportunity to improve the living conditions of EU citizens, both economically and environmentally. Pursuing this process in a challenging geopolitical environment will require decision-makers to be bold and forthright in their communication, able to prioritise, and determined to finish what they started.

About the author

Szymon Kardaś is a senior policy fellow on energy within the European Power programme, based in ECFR’s Warsaw office. His analysis focuses on the geopolitics of Europe’s new energy environment.

Acknowledgments

The author would like to thank experts and people working in the energy sector in institutions and companies in Poland, but also some other EU countries, for discussions on the topic covered in this policy brief. Special thanks are also due to those who provided comments on the first version of the text, in Mats Engström. The author would particularly like to thank Kim Butson for her pleasant and fruitful collaboration in editing the final version of the text, especially for her very valuable suggestions, questions, and comments. Thanks are also due to Nastassia Zenovich for the beautiful graphics included in the text.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.

Source link